Smaller, active money managers have been out of the spotlight, but they are optimally positioned to become the heroes of post-pandemic investing.

Investing After the Pandemic

Even as vaccines present an opening to our post-pandemic future, the investing world is fraught with uncertainty. Each major asset class presents a conundrum. Cash yields are close to zero thanks to more than a decade of policy intervention. Bonds, coming off the lowest yields in financial market history, offer the dangerous prospect of “return-free risk.” Rising rates and the specter of inflation recently triggered the worst dive in Treasury bond prices in 40 years. Moreover, deteriorating credit quality and profligate issuance raises repayment doubts for a wide variety of debt. Stocks are equally perilous: Buoyed by the post-2008 era of easy money, lofty valuations have made the market a fickle master. A case in point: the record-breaking, rapid decline of March 2020, followed by a historic, stimulus-led rally.

How can investors achieve returns, mitigate risk, and reach their goals moving forward? Amidst economic and market forces that appear larger than any of us, smaller may be better. Boutique asset managers, an eclectic and exceptional group of nimble specialists, possess a proven record of outperforming both market indexes and the titans of asset management — especially during periods of heightened volatility. Lately boutiques have been out of the spotlight, but they are optimally positioned to become the heroes of post-pandemic investing.

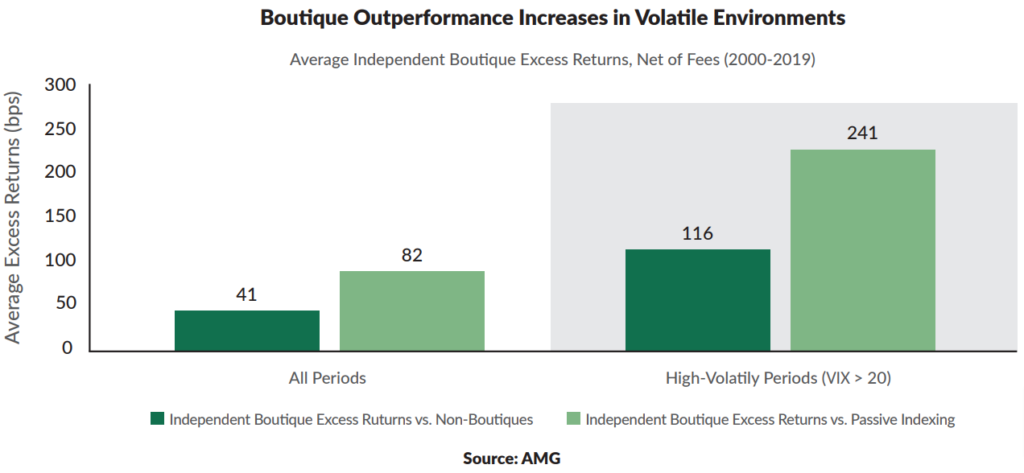

Several large-scale studies have delivered convincing evidence of the boutique advantage across geographic regions, asset classes, and investment styles, including both long-only and long-short strategies. A 2020 study of more than 1,300 individual investment management firms around the world and nearly 5,000 institutional equity strategies conducted by global asset manager Affiliated Managers Group (AMG) showed that independent, active boutique managers outperformed both non-boutiques and index investing in the 20-year period ending December 31, 2019. The excess annual returns over indexes, net of fees, averaged 82 basis points.1

These excess returns can drive significant additional wealth accumulation over time

Amidst economic and market forces that appear larger than any of us, smaller may be better.

During years of elevated market volatility, AMG found that boutique returns were distinctly higher, averaging 241 basis points of excess annual returns over indexing. Against traditional active managers, boutiques generated 116 basis points of excess returns during volatile periods. High volatility translates into higher dispersion of returns among securities. Thus, in volatile markets, according to AMG, skilled boutique managers “have been able to discern the most significant alpha generation opportunities and distinguish themselves.”2 When the going gets tough, boutiques get going.

1 “The Independent Boutique Advantage in Volatile Markets,” Affiliated Managers Group, Inc. Available at: https://amg.com/the-boutique-advantage.html.

2 Ibid.

Seven Characteristics of Boutique Managers

What is a boutique? And which of their characteristics help drive superior investment outcomes? Every boutique manager “starts with a story.” The insight and passion of one or more founders leads to their first portfolio. Then comes a spartan office space and the first employee. Dedication and a disciplined investment approach lead to something bigger. Yet the founders and their team remain undeterred in the pursuit of alpha generation.3

Although precise definitions vary, boutique asset managers tend to share seven common characteristics, as follows:

Small. Boutiques tend to manage a small amount of capital, typically less than $10 billion in assets, though the defining amount can vary depending on the strategy or the observer. That’s a far cry from large institutional managers that today may oversee $1 trillion or more in assets.

Owner-led. Principals and their investment teams often hold significant ownership in their firms, with compensation and personal net worth inextricably bound to performance. This “skin in the game” creates a powerful alignment of interest with investors. Shared ownership at boutiques also helps retain exceptional talent.

Specialized. Boutiques are specialists, with an expertise in one or a few market segments. This focus is a key driver

Unburdened by bureaucracy, boutiques can be more creative and make quick decisions.

of boutique outperformance, compared to larger firms offering a diffuse range of strategies and a shared (diluted) research platform. As specialists, boutiques prefer to be asset managers rather than asset gatherers, pursuing performance and avoiding a swollen asset base that may dampen results.

Lean. Boutique asset managers generally have a lean staff focused almost entirely on investment management. As a result, many back office and business functions such as accounting, legal, compliance, and distribution may be handled by third parties. Boutiques focus on what they do best and what drives results, and often outsource much of the rest.

Agile. Boutique managers are often nimbler than their larger counterparts. Unburdened by bureaucracy, they can be more creative and make quick decisions. Free from asset bloat, they can trade more quickly and effectively. Being small and agile enables boutiques to build concentrated, high-conviction portfolios rather than running closet indexing strategies like some larger active managers.

Accessible. Manager access is critical for allocators or investors who seek to understand a boutique manager’s strategy and how it fits within an investor’s overall portfolio. The ability to speak one-on-one with the portfolio manager differentiates the boutique experience from the largest asset managers.

Personal. Boutique managers generally know their investors personally. They experience the good times and tough times alongside their clients.

3 Johnson, Scott and Pickert, Joe, “Potential Advantages of Boutique Investment Firms Managing Mutual Fund Portfolios,” December 2017. Available at: https://buffalofunds.com/potential-advantages-of-boutique-investment-firms/.

A Global Edge

There is significant evidence that the boutique advantage transcends geographic boundaries, cutting across both traditional and alternative strategies.

A 2020 paper by Andrew Clare, Professor of Asset Management at the City University of London, examined the European fund management industry for the period starting in 2007. “Is There a Boutique Asset Management Premium?” answered Professor Clare’s own question by quantifying the differential in European mutual fund data: Compared to indexes, he found, European boutique managers outperformed by 82 basis points per annum gross of fees and 56 basis points per annum net of fees.4

Compared to “mega funds” offered by large active managers and adjusted for risk factors,

Boutiques outperformed by 52 basis points per annum gross of fees and 23 basis points per annum net of fees.

boutiques outperformed by 52 basis points per annum gross of fees and 23 basis points per annum net of fees. Outperformance was particularly pronounced in the European mid/small cap and emerging market equity sectors, according to Clare.5

Fidante Partners, a multi-boutique asset manager in Australia and a division of ASX-listed Challenger Limited Group, confirmed “The Boutique Advantage” in their paper on the Australian fund management industry. Fidante found that Australian boutique equity managers outperformed their benchmarks by 2.7% per annum net of fees in the ten years ending April 2017, with outperformance persistent across the three-, five-, seven-, and ten-year trailing periods. Fidante noted that “boutiques are higher conviction investors, taking more active risk compared to non-boutiques,” with the active risk “rewarded by higher realized returns and information ratios.” .6

Within the hedge fund universe, the outperformance of smaller managers is well documented. Beachhead Capital completed one of the seminal studies on the topic in 2013.

The study examined performance for 2,827 long/short equity hedge funds “drawn from the HFR database of live and dead funds.” Among the quick and the dead, smaller hedge funds outperformed consistently and returned 220 basis points per annum more than their larger peers in the decade of the study.7

Moreover, small managers outperformed before and after the financial crisis, and did not lag larger hedge funds during the crisis, “which may reflect superior risk management or a more manageable capital base,” according to the study’s authors.8

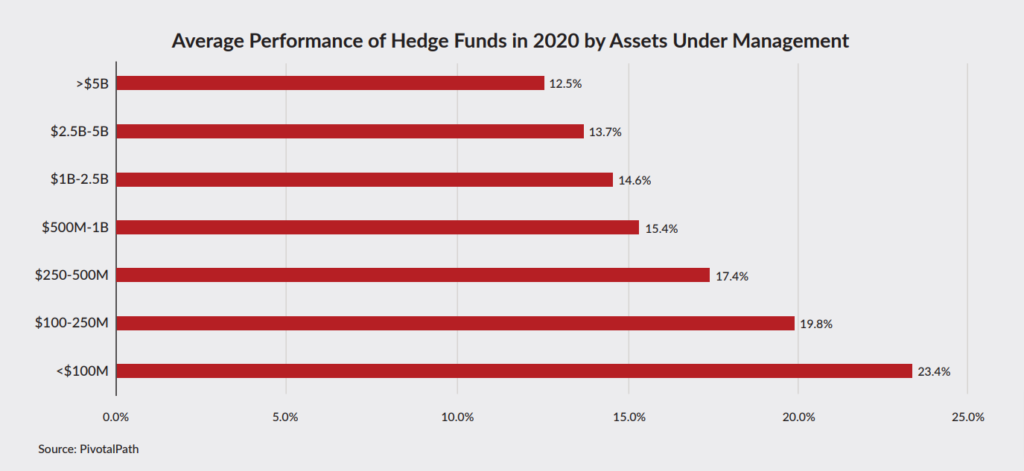

Findings from hedge fund researcher PivotalPath in 2020 were no different. Smaller hedge funds outperformed, they found. The average hedge fund with less than $100 million of assets under management (AUM) gained 23.4%, while the largest hedge funds, with more than $5 billion of AUM, gained 12.5% — little more than half the small hedge funds.9 “It’s so monotonic,” Jon Caplis, CEO of PivotalPath, told Institutional Investor. “The larger you are, the worse you do. The smaller you are, the better.”10

4 Clare, Andrew D., “Is There a Boutique Asset Management Premium?,” February 21, 2020. Available at: https://ssrn.com/abstract=3542243 or http://dx.doi.org/10.2139/ssrn.3542243.

5 Ibid.

6 Hamilton, Nick and Kretschmann, Michael, “The Boutique Advantage,” 2017. Available at: https://www.fidante.com/-/media/Fidante/resources/Articles/FIDA-The-Boutique-Advantage.ashx.

7 “Smaller Hedge Fund Managers Outperform: A Study of Nearly 3,000 Equity Long/Short Hedge Funds,” AllAboutAlpha. Available at: https://www.allaboutalpha.com/blog/2013/02/18/smaller-hedge-fund-managers-outperform-a-study-of-nearly-3000-equity-longshort-hedge-funds/.

8 Ibid.

9 “Pivotal Indices,” PivotalPath, December 2020.

10 Segal, Julie, “Large Managers Get the Money, but Small Managers Provide the Performance,” Institutional Investor, October 15, 2020. Available at: https://www.institutionalinvestor.com/article/b1ntn371zfynmz/Large-Managers-Get-the-Money-but-SmallManagers-Provide-the-Performance.

Due Diligence Considerations

Although the performance case for boutiques is compelling, selecting the right boutique manager is not without challenges. Dispersion of returns can be high, and committing to a lagging boutique may be frustrating. A concentrated portfolio or narrow style may lead to bouts of underperformance when the boutique is out of sync with the broader markets. The challenge grows if a boutique manager utilizes exotic instruments: Investors must then ascertain if the manager has the appropriate guardrails in place. Understanding the risks of a boutique manager is paramount.

Boutiques may also lack the infrastructure or scale to win large mandates from institutions such as endowments, foundations, and pension funds, or earn slots on major retail brokerage platforms. To scale efficiently and effectively while retaining their edge, boutiques require the right partners to build compliance systems, trading infrastructure, marketing, and distribution.

Proper due diligence of the boutique landscape requires a careful assessment of the risks, idiosyncrasies, and infrastructure. Still, the track record of this nimble and idiosyncratic class of active managers seems purpose-built for the post-COVID market environment, especially given their knack for delivering enhanced returns during periods of heightened volatility. The data and research point to a winning formula: When boutiques focus on what they do best, the alpha often follows.

Boutiques require the right partners to build compliance systems, trading infrastructure, marketing, and distribution.

Warren Buffett and Boutiques

Early in his career, Warren Buffett was a boutique manager of small private investment partnerships. After merging the partnerships into one, Buffett began buying shares of a small, struggling textile manufacturing company, Berkshire Hathaway. Buffet gained control of Berkshire and ultimately transformed it into a multinational conglomerate and holding company. The resulting wealth creation forever changed the fortunes of his early investors.

Nonetheless, Berkshire Hathaway has struggled in more recent years to keep pace with the markets. A dollar invested in 2009 was worth $2.40 by 2019, versus $3.20 for the S&P 500.10 In 2019 and 2020, Buffett trailed the S&P 500 by a combined 37%.11

Mr. Buffett shares a fate akin to that of the largest asset managers. Running gargantuan sums of money can often mean convergence with, or underperformance relative to, market indexes. Large asset managers are therefore either honest providers of beta competing as low-cost providers, or closet indexers seeking to retain assets as outflows erode their franchise — or they must seek to match the returns of smaller, nimbler boutiques with a specialized strategy.

10 Armstrong, Robert, Platt, Eric, and Ralph, Oliver, “Warren Buffett: ‘I’m having more fun than any 88-year-old in the world,” Financial Times, April 25, 2019. Available at: https://www.ft.com/content/40b9b356-661e-11e9-a79d-04f350474d62.

11 Rosenbaum, Eric, “What Warren Buffett’s losing battle against S&P 500 says about this market,” CNBC.com, January 8, 2021. Available at: https://www.cnbc.com/2021/01/08/how-warren-buffetts-uphill-battle-against-the-sp-500-is-changing.html.